US Economic Outlook

The US economy continued to appear resilient on the surface through the third quarter of 2025, supported by steady consumer spending and a low unemployment rate. Beneath the headline numbers however, the labor market has meaningfully weakened. From January through April, monthly job gains averaged 123,000 but slowed sharply to just 27,000 per month from May through August. Monthly job growth in 2025 has significantly underperformed both expectations and the 2011-2019 pre-pandemic average of 194,000.

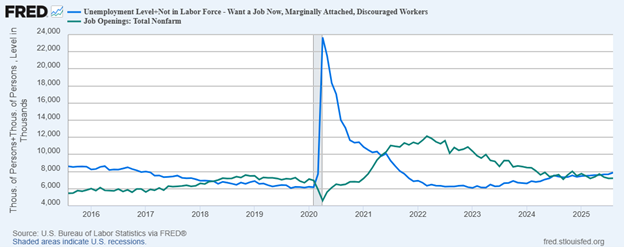

A key shift has been in job openings. The ratio of job postings to unemployed persons fell below 1.0 in the third quarter for the first time since 2021, indicating more job seekers than available jobs. When factoring in those not currently in the labor force or actively looking but willing to work, that ratio has been below parity for most of 2025. Job openings have steadily declined from their 2022 peak, while unemployment has trended higher since early 2023. This softening points to a labor market losing momentum.

A declining labor force participation rate has given the illusion of stable and low unemployment, with the unemployment rate hovering around 4% for over a year, despite the rising number of unemployed. However, the unemployment rate climbed to 4.3% in August, the highest since October 2021. A widening spread between job openings and unemployed persons may cause the unemployment rate to rise further.

Long-term unemployment is also rising, with individuals unemployed for 27 weeks or longer accounting for 25.7% of all unemployed in August. This is higher than pre-pandemic levels and is roughly four percentage points higher than a year ago. Together, these shifts indicate fewer available opportunities, slower job creation, and increasing strain on wage growth and household stability.

Consumer spending rose for the third straight month in August, but the strength is a less reliable indicator of aggregate consumer health as consumer spending is increasingly concentrated among upper-income households. According to Moody’s Analytics, the top 10% of earners (income above $250,000) now account for nearly 50% of all spending. As consumption represents roughly 70% of GDP, this group alone drives approximately one-third of economic output.

Outside this cohort, household finances continue to deteriorate. Wage gains are slowing, especially for lower-income workers, while personal income growth is lagging consumption. Personal spending rose 0.6% in August and 0.5% in July month-over-month, outpacing personal income growth of 0.4% in both months. Consumers are increasingly relying on credit cards, personal loans, and buy-now-pay-later arrangements to maintain spending levels. Total household debt reached $18.4 trillion in the second quarter, or $105,000 per household, up 13% since 2020.

The concentration of spending among high earners is masking growing financial strain elsewhere in the economy. If sentiment among this group weakens or if income gains slow further across the broader population, consumer spending and economic growth could soften heading into 2026.

Inflation remains elevated near 3%, still above the Federal Reserve’s 2% target. With the labor market weakening, the central bank now finds its dual mandate of stable prices and maximum employment in conflict. Because of increased downside risks to the labor market, the Fed delivered two 25 basis point rate cuts in September and October, lowering the federal funds rate to 3.75–4.00%. The last time the Fed funds rate was below 4.0% was at the end of 2022.

While Fed officials previously signaled one additional rate cut by year-end, the path is now less certain. The Fed is balancing still elevated inflation against growing evidence of labor market slack. The policy stance has shifted from “higher for longer” to “easing when warranted”.

The Commercial Real Estate Landscape

Commercial real estate remains in a delicate balance. Economic growth is moderating, inflation and borrowing costs remain elevated, new supply is still entering several markets, and a historic volume of loan maturities looms. Underwriting has become more conservative and refinancing remains challenging. However, there are signs of stabilization and easing monetary policy is expected to provide additional relief.

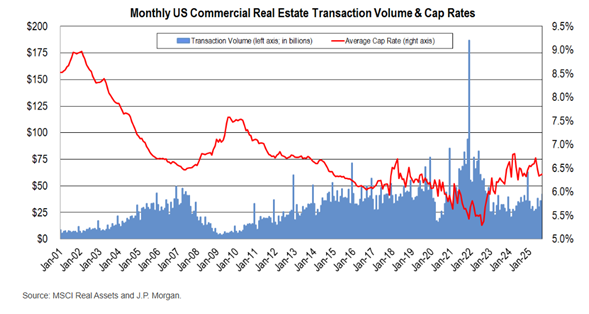

MSCI Real Assets reported that September sales volume rose 19% year-over-year, led by a rebound in office trades. JPMorgan estimates that third quarter transaction volume reached nearly $124 billion, or a 16% year-over-year increase, with potential upward revisions as high as $140 billion.

Despite the increased activity, transaction volume still pales in comparison to the scale of upcoming maturities of more than $2 trillion through 2027, including nearly $1 trillion in 2025 alone. Additionally, valuations have stabilized but remain 15–20% below peak 2021–2022 levels according to Green Street’s CPPI. Pricing is holding steady primarily because many owners continue to pursue loan extensions or modifications rather than transact at discounts that would reset valuations.

CMBS delinquencies have plateaued around 7.2%, up 153 basis points year-over-year. Office continues to be the most challenged sector at 11.1%, while multifamily delinquency has doubled to 6.6%. Although delinquency levels appear stable quarter-to-quarter, the distribution across property types highlights the uneven recovery.

Interest rates will continue to define the trajectory for commercial real estate. Lower interest rates should offer relief for floating rate borrowers, improve the ability to refinance existing loans and reduce the bid-ask spread between buyers and sellers.

The Alpha Investing Strategy

Despite heightened macro uncertainty, we continue to believe in the long-term fundamentals of commercial real estate. We are actively evaluating acquisition opportunities but remain highly selective. Our strategy remains grounded in fundamentally sound real estate with outsized upside potential relative to the downside risk. We focus on assets with strong in-place cash flow, conservative capital structures, fixed-rate or hedged debt, and clear paths for value creation.

In an environment where cap rate spreads to borrowing costs remain compressed, we continue to emphasize downside protection and selectivity. Lower interest rates may unlock additional investment opportunities, but we expect transaction volume to remain muted in the near term as owners prioritize loan modifications and extensions over sales. Additionally, CBRE notes that cap rates appear to have peaked in early 2025 and are drifting lower, which would erode some of the risk-premium benefits of falling interest rates.

Senior housing continues to stand out as one of the most compelling opportunities in today’s market due to sector fundamentals and higher going-in yields. Demand is accelerating as the 80+ population expands, while new supply remains highly constrained. NIC projects a 550,000-unit shortfall by 2030. Additionally, operational complexity and a fragmented ownership base create opportunities for experienced operators to drive meaningful value through efficiency, scale, and management improvements.

We continue to evaluate other asset types and investment strategies, including single-tenant net lease (STNL). These investments offer durable, credit-anchored income streams with limited operating risk. Tenants are responsible for the majority of operating expenses and typically sign leases with 10–20+ years of term. With conservative leverage and fixed-rate debt, STNL investments can provide stable income and attractive risk-adjusted returns in today’s environment. Alpha Investing closed on a STNL transaction at the end of the third quarter.

Across our existing portfolio, our focus remains on proactive asset management to strengthen operations, stabilize income, and preserve optionality as the market works toward equilibrium. We continue to pursue loan modifications where appropriate, add protective capital when necessary, and prioritize operational improvements that enhance NOI and long-term value.