US Economic Outlook

The U.S. economy showed increasing signs of stress in the second quarter, with consumer spending moderating and the labor market experiencing a sharp slowdown. Although headline GDP growth came in at an annualized rate of 3.0%, according to the initial estimate, rebounding sharply from a 0.5% contraction in the first quarter and exceeding market expectations, much of the increase reflects timing effects from tariffs rather than underlying domestic demand.

Imports surged by 40% in the first quarter as businesses and consumers accelerated purchases ahead of anticipated tariff increases, which subtracted roughly 4.7 percentage points from GDP. In the second quarter, imports fell 30% as companies worked through elevated inventories, contributing positively to GDP. Core domestic demand, excluding net exports, remained subdued. Private fixed investment contracted, and consumer spending rose at a modest 1.4% pace, with stronger-than-expected June retail sales helping to offset a slower start to the quarter. It remains to be seen whether June’s performance reflects a broader trend of resilience or a one-off increase.

Consumer spending, which accounts for nearly 70% of GDP, is increasingly concentrated among higher-income households. According to Moody’s Analytics, the top 10% of U.S. households (those earning $250,000 or more annually) now account for nearly half of all consumer spending. By comparison, in 2019, it took the top 27% of the consumer base to reach 47% of total consumer spending, according to Visa’s Business and Economic Insights. Spending power has become significantly more concentrated. Over the past four years, spending by the top 10% has increased by 58%, compared to 25% for the bottom 80% of earners, which has barely kept up with inflation of 21%. When paired with record levels of household debt, this data suggests middle- and lower-income consumers are already financially strained and will face increasing pressure from inflation. A decline in sentiment or spending among high-income households could have an outsized impact on consumption and economic growth.

The labor market showed clear signs of deceleration in the second quarter, with job growth slowing sharply. After averaging 111,000 monthly gains in the first quarter, job creation slowed to just 64,000 per month in the second quarter, following large downward revisions to both May and June totaling 258,000 jobs. May’s job growth was estimated to be 19,000, and June just 14,000. This marks a significant and sustained slowdown from 2024 and 2023, when average monthly job gains were 168,000 and 216,000, respectively. While the unemployment rate remained steady between 4.1% and 4.2%, and wage growth continues to outpace inflation, the hiring trend points to a labor market that is clearly weakening.

After easing for much of the year, inflation picked up notably in June, raising concerns that price pressures may be reaccelerating, particularly as the effects of recent tariffs continue to work through the system. As of quarter-end, the average effective tariff rate had risen to 18%, a significant increase from the 2024 average of 2.5%. While the U.S. has reached new trade agreements with several countries, negotiations remain ongoing with other key trading partners, including China.

The Federal Reserve has indicated that, absent the inflationary effects of new trade policy, rate cuts might have already commenced. However, the uncertainty surrounding tariffs and their impact on inflation and growth has complicated the Fed’s outlook. As of June, the median FOMC projection called for two 25-basis-point cuts in the second half of the year. In July, the Fed held the federal funds rate steady at 4.25%–4.50% for a fifth consecutive meeting, prior to the sharp downward revisions to May and June employment data. Notably, two of the 12 voting members dissented, voting in favor of a rate cut. This marks the first time in over three decades that two Federal Reserve Board Governors have voted against the chair. The Fed continues to weigh the competing risks of inflation and slowing growth. The sharper-than-expected slowdown in job creation may weigh on the Fed’s outlook and support the probability of rate cuts in the second half of the year

The Commercial Real Estate Landscape

The commercial real estate sector continues to face headwinds in 2025, including elevated operating costs, high interest rates, new supply, and a historic volume of loan maturities. While some pressures were expected to ease, policy uncertainty, particularly around trade and immigration, has contributed to deteriorating sentiment related to inflation, employment, and financial stability.

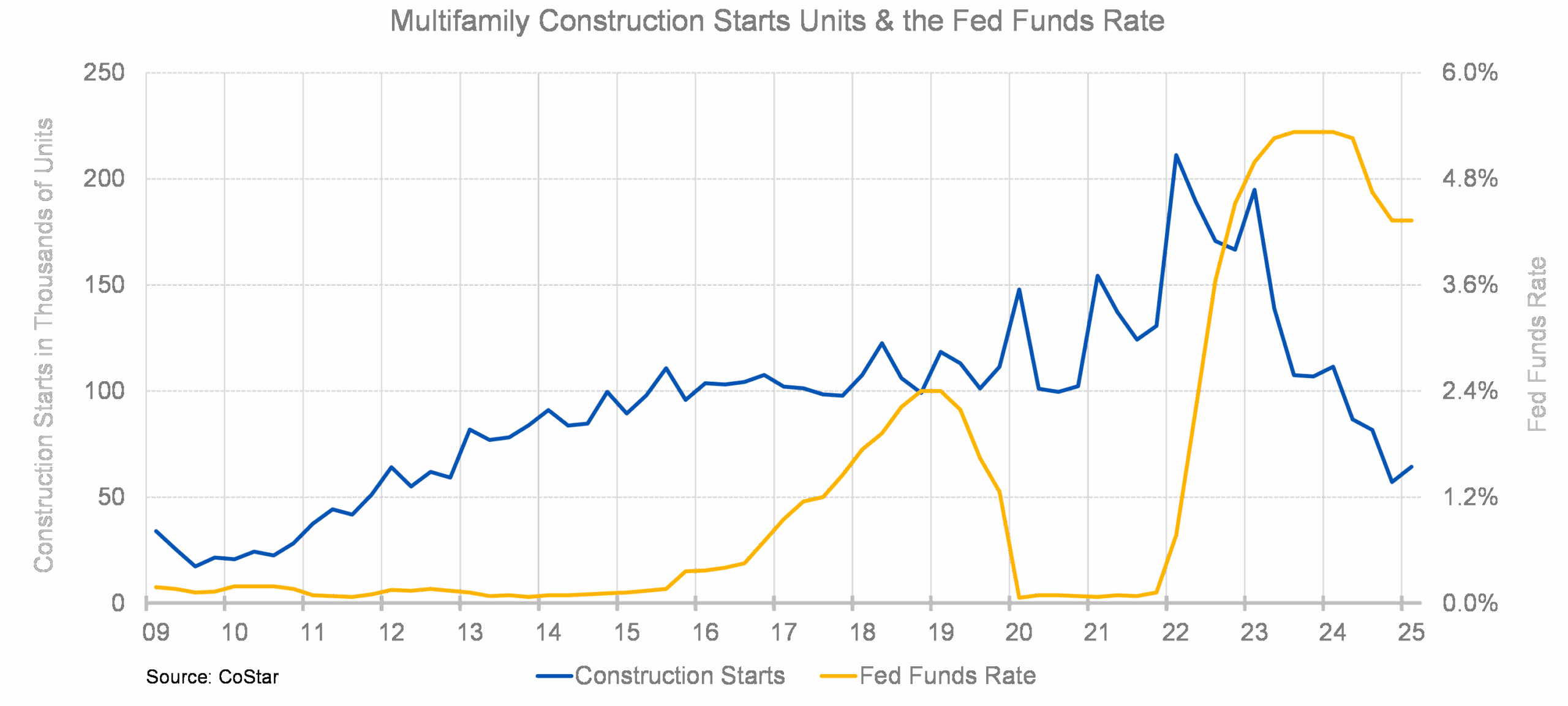

Tariffs and restrictive immigration policy may reignite inflationary pressures, driving operating costs higher. However, those same pressures are likely to dampen future construction. Multifamily deliveries remain elevated in 2025, but construction starts have declined sharply from their 2022 peak. Rising interest rates, construction costs, and macro uncertainty have delayed or sidelined many new projects. According to CoStar, multifamily deliveries are projected to fall roughly 40% in 2025 and another 35% in 2026, tightening supply-demand fundamentals in future years.

While the surge in new supply during 2023 and 2024 led to higher vacancies and limited rent growth, multifamily demand has remained resilient. Affordability challenges continue to weigh on homeownership. In the second quarter, the national homeownership rate declined to 65%, nearly 3 percentage points below the recent peak of 67.9% in the second quarter of 2020 and below the 25-year average of 66.3%. With elevated mortgage rates and rising home prices, multifamily remains a critical alternative for many households.

Commercial real estate transaction and lending activity have improved, and pricing appears to be stabilizing. Sales volume has increased year-over-year for five straight quarters. That said, first-half 2025 transaction volume totaled just $133 billion, per CoStar, which pales in comparison to the more than $1.1 trillion in commercial real estate debt maturing this year.

A persistent bid-ask spread between buyers and sellers continues to constrain deal flow. Buyers are pricing assets based on higher borrowing costs, while many sellers remain anchored to legacy valuations. When faced with an upcoming debt maturity, borrowers typically refinance with a new loan or sell the property to repay the loan. For many owners facing loan maturities, refinancing remains difficult due to the spread between current interest rates and those on their maturing loans. Rather than forcing distressed sales, lenders continue to extend and modify existing loans. Of the $1.1 trillion in 2025 CRE maturities, roughly $520 billion represent extensions from prior years. As long as lenders remain accommodative, forced sales and price capitulation are likely to remain limited.

The Alpha Investing Strategy

Despite heightened macro uncertainty, we continue to believe in the long-term fundamentals of commercial real estate. We remain active in evaluating acquisition opportunities, though we remain highly selective, targeting fundamentally sound real estate with outsized upside potential relative to the downside risk. We focus on assets with downside protection through strong and durable in-place cash flow, fixed-rate debt or rate caps, and business plans that offer a clear path to value creation. While cap rates have moved modestly higher in recent quarters, they remain compressed relative to the rise in interest rates. Our approach emphasizes disciplined underwriting and proactive asset management to generate attractive risk-adjusted returns.

Senior housing continues to stand out as a particularly compelling opportunity. Demand is growing rapidly as the 80+ population expands, while new supply remains highly constrained. Even before tariffs threatened to increase construction costs, there was already a material shortage of units in the senior housing development pipeline. According to NIC, the sector faces a projected shortfall of 550,000 units by 2030. Furthermore, senior housing’s operational complexity and fragmented ownership structure create acquisition opportunities for investors partnered with experienced operators to acquire assets at attractive pricing and drive meaningful value creation through better management and operational efficiencies.

We continue to evaluate other asset types and investment strategies. Specifically, we are actively pursuing opportunities in the single-tenant net lease (STNL) space. Tenants are responsible for the majority of operating expenses and typically sign leases with 10–20+ years of term. These assets offer limited operating responsibilities, long-term lease stability, and predictable cash flow when acquired with conservative leverage and fixed-rate debt. While tenant credit quality must be evaluated carefully, many STNL tenants carry investment-grade ratings. In the current environment, we view select STNL investments as attractive opportunities.

Like the broader commercial real estate sector, a portion of our portfolio includes floating-rate debt with near-term maturities. We continue to focus on securing holding power through loan modifications, capital infusions, and operational improvements. Across our portfolio, we remain focused on optimizing asset operations and improving NOI to maximize value.