US Economic Outlook

US economic growth remained resilient through the fourth quarter of 2025, but underlying indicators continued to weaken. Consumer confidence declined for a fifth consecutive month, driven by concerns around the labor market, persistent inflation, and financial conditions that remain restrictive despite recent interest rate cuts.

Across multiple measures, the labor market showed clear signs of cooling. While the unemployment rate held within a narrow range of 4.0–4.3% through much of the first half of the year, it edged higher to 4.4–4.5% by year end. More concerning than the headline unemployment rate, however, is the deterioration beneath the surface. In total, 584,000 jobs were added in 2025, averaging just 49,000 per month, a sharp deceleration from 2024’s average of 168,000 monthly job gains. Job growth was also weaker than initially reported, with downward revisions totaling 646,000 over the course of the year. Given the pattern of revisions, November and December employment figures may be revised lower in the coming months as additional survey data becomes available.

At the same time, layoffs accelerated materially. According to Challenger, Gray & Christmas, 2025 job cuts exceeded 1.2 million, the highest level since 2020 and 58% higher than in 2024. Notably, layoffs resulted in three months of net job losses during the fourth quarter.

Long-term unemployment also increased meaningfully. Individuals unemployed for 27 weeks or longer accounted for roughly 26% of all unemployed workers in December, which exceeds pre-pandemic levels and is 3.6 percentage points higher than a year earlier. These trends suggest that job losses are becoming more persistent and re-employment is growing more difficult. These conditions typically exert downward pressure on wage growth and consumer confidence.

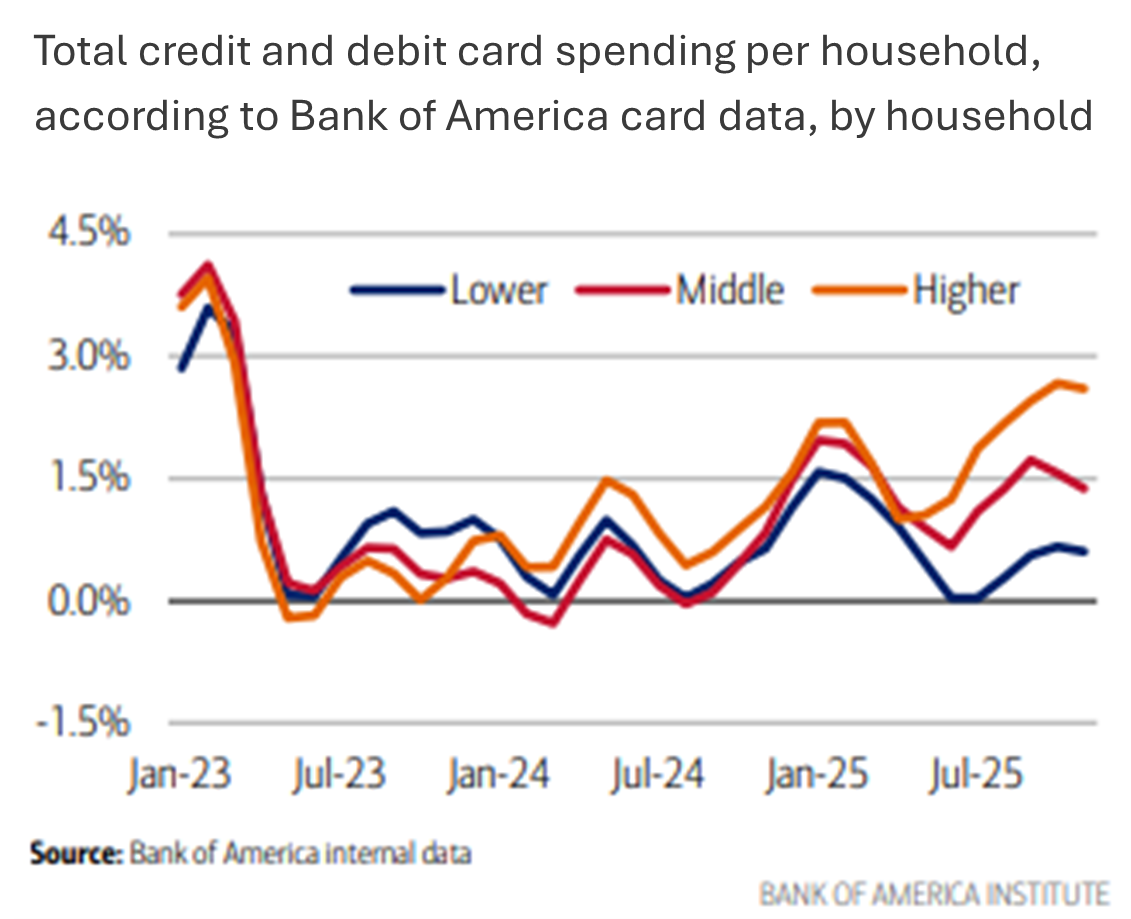

Consumer spending remained strong in aggregate, but the increasingly K-shaped nature of the economy continues to mask weakness across much of the population. Higher-income households continued to increase spending, while lower-income consumers pulled back. According to Bank of America data, higher-income households maintained spending growth of 2.6% year-over-year, while lower-income spending grew by just 0.6%. Wage growth decelerated through the second half of the year and, for many households, failed to keep pace with inflation.

The divergence is evident in the automotive market. New vehicle prices reached record highs in 2025, with the average transaction price surpassing $50,000, driven largely by high-income consumers purchasing larger and more expensive vehicles. Despite record pricing, total sales volume reached a six-year high, as higher-income consumers more than offset pullbacks elsewhere. Households earning over $150,000 accounted for 43% of new vehicle purchases in 2025, up from 33% in 2019, according to Cox Automotive. At the same time, auto loan delinquencies, defaults, and repossessions rose sharply, approaching levels last seen during the 2008 financial crisis, underscoring growing financial strain among lower- and middle-income households. The concentration of spending among higher-income consumers has supported economic growth to date, but this dynamic remains increasingly sensitive to shifts in sentiment and asset markets.

Inflation remained elevated near 3% throughout the year, above the Federal Reserve’s long-term 2% target, but largely avoided the tariff-driven spikes many economists initially feared. Goods inflation has largely normalized, while services inflation has remained persistent. In response to moderating growth and a weakening labor market, the Federal Reserve shifted toward guarded monetary easing, delivering three consecutive 25 basis point rate cuts in the final FOMC meetings of the year, bringing the target federal funds rate to 3.5–3.75%. These cuts reflect risk management rather than economic stimulus.

Looking ahead, monetary policy remains uncertain. At its first meeting of 2026, the Fed left the federal funds target rate unchanged and reiterated that future easing will be gradual and data dependent as it balances a weakening labor market against inflation that remains above target. Disagreement among policymakers has become more persistent, with dissent recorded in the last four FOMC meetings. While short-term rates have moved lower, longer-term rates remain elevated. The 10-year Treasury, which reflects broader economic, fiscal, and geopolitical risk, has been volatile and slow to decline and is likely to remain higher than investors would prefer, limiting the transmission of rate cuts into lower borrowing costs across the economy.

The Commercial Real Estate Landscape

Commercial real estate experienced a year of tepid stabilization in 2025 as monetary policy shifted from restrictive to cautiously accommodative. Market conditions improved at the margins, transaction activity increased, and pricing appeared to stabilize across many sectors. However, weaker labor market conditions, slowing economic growth, elevated borrowing costs, and a historic volume of near-term debt maturities continue to weigh on performance and sentiment.

The dominant theme in commercial real estate remains refinancing risk. Approximately $1 trillion of CRE debt was set to mature in 2025, nearly triple the 20-year average. While values have largely stabilized, they remain meaningfully below peak 2021–2022 levels due to cap rate expansion and, in some cases, lower operating income. This has made both asset sales and refinancing challenging, particularly for properties acquired at or near peak pricing. Although transaction activity has increased, it remains dwarfed by the scale of upcoming maturities, as many owners continue to pursue loan extensions, modifications, and recapitalizations rather than transact and realize losses.

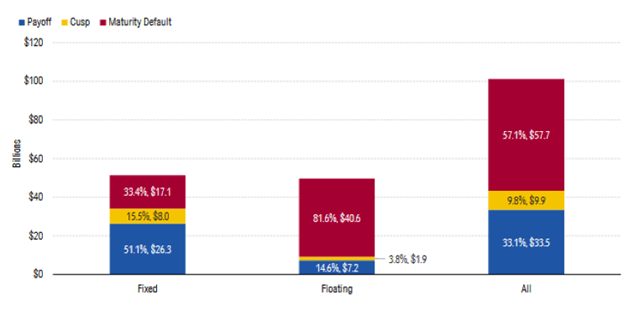

CMBS delinquency climbed steadily throughout the year, ending 2025 at 7.3%, up 73 basis points year-over-year. Delinquency surpassed 7% in April, its highest level since January 2021, and remained elevated for the remainder of the year. Delinquency remains concentrated in office and, increasingly, in certain segments of multifamily, where new supply, slowing rent growth, and higher operating costs have compressed margins. While these levels are not yet indicative of widespread distress, they underscore the difficulty of working through the maturity wall in an environment where capital remains available but expensive. Of the approximately $100 billion in CMBS loans maturing in 2026, an estimated 57% are at risk of default at maturity, according to Morningstar.

Looking into 2026, the commercial real estate market is likely to remain uneven and opportunity-driven as the market works through refinancing challenges and transitions toward a more sustainable equilibrium.

The Alpha Investing Strategy

Against a backdrop of slowing economic growth, a cooling labor market, and easing, but still elevated, interest rates, our investment approach remains disciplined and selective, focused on fundamentally sound real estate with outsized upside potential relative to downside risk. We believe this phase of the cycle can create opportunities for well-capitalized investors and operators with operational expertise and a long-term perspective.

Our primary focus remains on assets with durable in-place cash flow, conservative capital structures, fixed-rate debt or rate caps, and clear paths to value creation that do not rely on aggressive rent growth or cap rate compression. Even as borrowing costs decline modestly, the spread between cap rates and Treasury yields remains compressed by historical standards. In 2025, the 10-year Treasury yield largely remained in the 4.0–4.5% range, which is significantly higher than the 2.0% average from 2010-2021, before the Fed’s aggressive rate tightening cycle began in March 2022. Cap rates have not expanded nearly as much. As a result, we continue to underwrite transactions assuming limited multiple expansion and prioritize current cash yield and operational improvement as primary drivers of return.

We remain cautious on sectors where fundamentals have not fully reset. Multifamily continues to face near-term pressure from record new supply, slowing rent growth, elevated vacancies, and rising operating costs. While long-term demand drivers remain intact, supported by high homeownership costs, current pricing in many markets does not yet provide sufficient margin of safety.

We see compelling opportunities in sectors where structural demand is accelerating and supply remains constrained. Senior housing continues to stand out as one of the most attractive risk-adjusted opportunities. Rapid growth in the 80-plus population is colliding with years of underdevelopment, while operational complexity and fragmented ownership have limited institutional capital. These dynamics create opportunities for experienced operators to acquire assets at attractive bases and drive meaningful value through improved management, staffing, and operating efficiency.

We also continue to evaluate other asset types and strategies, including select single-tenant net lease (STNL) opportunities that offer long-term, credit-anchored income with limited operating risk. In an environment with reduced economic visibility, assets with long lease terms, predictable cash flow, and tenants responsible for the majority of operating expenses, provide stability when combined with conservative leverage and fixed-rate debt.

In addition to equity investments, we are increasingly focused on structured capital solutions arising from the refinancing cycle. Loan modifications, preferred equity, and recapitalizations are becoming more prevalent as owners seek to bridge maturities in a higher rate environment. When structured appropriately and paired with strong sponsorship, these investments can offer compelling entry points and stable cash flow.

Across our existing portfolio, proactive asset management remains a priority. We continue to focus on optimizing operations, controlling expenses, strengthening tenant retention, and preserving liquidity. Where appropriate, we are working with lenders to extend maturities and improve capital structures to maintain flexibility in a slower-growth environment.

Looking ahead to 2026, we believe opportunities in commercial real estate will broaden, but unevenly. Markets will continue to differentiate between high-quality, well-capitalized assets and those burdened by leverage, weak fundamentals, or legacy valuations. Our strategy is to remain patient through this transition, deploy capital selectively where risk-adjusted returns are compelling, and position the portfolio to benefit as the market moves toward a more balanced phase of the cycle.